Most enterprise marketing plans for 2026 still read like a familiar playbook refresh: sharper ABM, better creative, more always-on, improved conversion, tighter intent, a new website release, a brand refresh. Useful work—inside the old physics.

But the biggest shift isn’t a tactic. It’s where buying begins.

Enterprise buyers are increasingly discovering, shortlisting, and pre-qualifying vendors (and every other category of enterprise tech) through LLMs and generative search—before your SDRs, partners, events, review sites, or demand programs ever get a chance to shape the narrative. And as that “first layer” of discovery consolidates into answers instead of clicks, market access is being re-priced.

The uncomfortable truth: “Search” is turning into “Answers”

Gartner put a big flag in the ground: by 2026, traditional search volume could drop meaningfully as people shift toward AI chatbots and virtual agents.

Whether you agree with the exact number or not, the direction is what matters: discovery is migrating from “ten blue links” to synthesized comparisons.

And the buyer-side adoption data is no longer hypothetical:

Forrester reports 89% of B2B buyers have adopted generative AI, and they use it as a self-guided information source across buying phases.

eMarketer (citing HG Insights) reports 47% of B2B buyers use AI for market research and discovery and 38% use it for vetting and shortlisting vendors.

6sense reports that buyers place most vendors on a “Day One” shortlist early—and in 95% of cases (in 2025) they ultimately buy from that initial shortlist.

If you’re a senior enterprise marketer, pause and connect the dots:

If the shortlist forms earlier… and buyers increasingly consult LLMs earlier… then your new primary KPI is not “clicks/visits.” It’s inclusion.

Inclusion in the answer. Inclusion in the shortlist. Inclusion in the category narrative.

Market access now happens before the funnel you measure

In the classic model, marketing created awareness → drove traffic → captured leads → influenced evaluation.

In the emerging model, the early journey looks more like:

Prompt → synthesized comparison → shortlist → internal alignment → only then… vendor engagement.

By the time your paid media, ABM ads, nurture sequences, webinars, and partner plays start firing, many buyers already have:

a mental model of the category,

a default ranking of vendors,

and a pre-built story about “who’s best for what.”

That story is increasingly being shaped by systems that reward what’s available, consistent, frequently repeated, and easy to summarize.

So here’s the thought that should keep you up:

Your brand doesn’t enter the funnel when the buyer visits your site.

Your brand enters the funnel when the model decides you belong in the answer.

Why this creates a structural disadvantage (especially for nuanced differentiation)

LLMs are not “fair.” They’re compressive. They flatten nuance into a few sentences. They generalize. They prioritize what they can corroborate across sources. And they tend to amplify the dominant narratives that exist “in the open.”

That’s fine if your differentiation is obvious and widely repeated. It’s deadly if your differentiation is:

complex (outcomes, architecture, TCO realities),

contextual (industry-specific value),

or locked inside internal decks, sales talk tracks, enablement docs, and partner conversations.

Because if your strongest differentiators aren’t legible to LLMs, they’re functionally invisible at the moment the buyer is forming their first shortlist. And invisibility at that stage is not a branding issue. It’s a market-access issue.

The compounding effect: how “invisibility” turns into structural decline

This is the part most teams underestimate. The downside isn’t a bad quarter. It’s a quiet flywheel of decay:

Organic traffic erosion If fewer buyers discover you through search or AI answers, fewer high-intent visitors land on your core pages.

Paid efficiency decay When organic and AI-assisted discovery underperform, paid has to “buy back” what you used to earn. Costs rise, targeting broadens, and waste creeps in.

Pipeline quality degradation You get more “curious” traffic and fewer “convinced” buyers. Sales spends more time re-teaching basics instead of advancing decisions.

Win-rate pressure Buyers enter evaluation with a pre-built frame. If that frame favors competitors, you’re now fighting gravity—often with discounting.

This is why 2026 is not a marketing upgrade cycle. It’s a market-access reset.

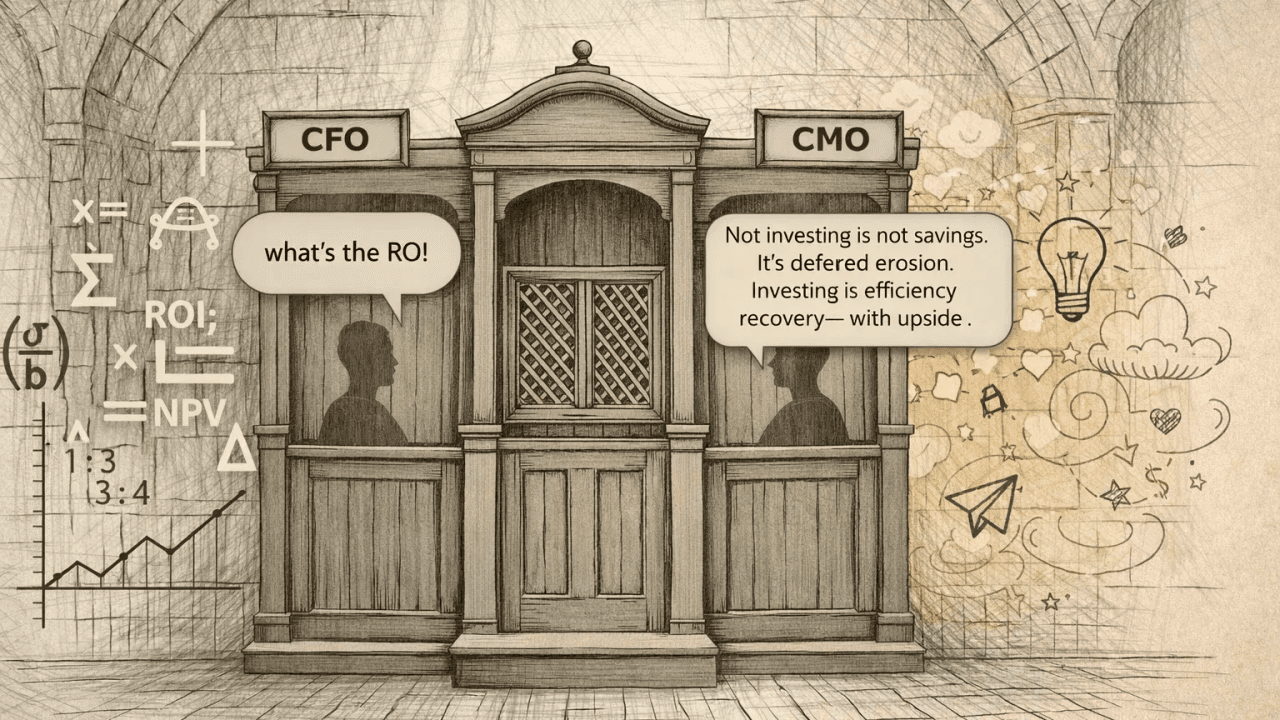

The CFO translation: not investing is not cost-neutral—it’s value destructive

Many organizations will treat “not investing” as conservative. It feels prudent: protect budget, keep doing what works, wait for clarity.

But in a market-access reset, not investing is an active choice to accept compounding efficiency loss.

Because the business doesn’t stand still:

discovery shifts upstream into AI answers,

your inclusion rate drops,

and your commercial system starts spending more to achieve the same output.

This is the hidden cost of “not innovating”: you don’t just miss upside—you absorb structural decline.

And that’s the ROI conversation most CFOs actually care about:

margin protection,

CAC protection,

sales efficiency protection,

win-rate protection.

Importantly, CFO skepticism about “AI initiatives” is justified—Gartner has warned that many hyped AI projects can fail due to high costs and unclear outcomes. So the answer is not “trust us, AI is the future.” The answer is: this isn’t speculative growth. It’s efficiency recovery.

Why the best ROI story in 2026 is efficiency recovery, not “growth experiments”

If you frame this as “new growth,” you invite the wrong debate: forecasts, attribution wars, and skepticism.

But if you frame it as efficiency recovery, the math becomes concrete:

Recover lost organic demand by restoring AI discoverability

Improve paid efficiency by reducing “buy-back” spend

Increase pipeline quality by shaping the narrative earlier

Improve win rates by entering evaluation with the right frame

That’s not fluffy. It’s unit economics.

This becomes a capital protection decision with upside—not a marketing experiment.

“More content” won’t fix this. A new operating model will.

A predictable reaction is: “Let’s publish more.”

But LLMs don’t reward volume. They reward:

clarity,

consistency,

corroboration,

and usefulness in the buyer’s language.

In other words: your job is no longer to “create campaigns.”

Your job is to encode market truth in a way that both humans and machines can reliably retrieve and summarize.

Think of it like this: Build a canonical knowledge layer → then generate every human and machine-facing asset from it.

What an LLM-first market-access model looks like (practically)

Here’s a pragmatic blueprint that enterprise teams can actually run—without turning marketing into a science project.

1) Create a canonical “Decision-Ready” layer One deep reference brief per market/industry (and micro-segment where it matters): category context, buyer pains, competitive framing, proof points, objections, product-to-outcome mapping, and “why us.”

This becomes the source of truth for:

web pages,

comparison pages,

FAQs,

analyst and partner toolkits,

sales enablement,

and the bite-sized assets executives actually consume.

2) Make differentiation machine-legible This is where most teams fail. They write beautiful messaging that humans understand but machines can’t anchor.

Machine-legible means:

explicit claims tied to evidence,

consistent terminology,

clear “vendor A vs vendor B” answers,

and structured pages that align with buyer questions.

3) Build corroboration beyond your own site LLMs triangulate. If your story only exists in your owned channels, it’s fragile.

You need external echoes:

partners,

customers,

credible third parties,

and repeatable proof points.

4) Measure “AI inclusion rate” and narrative share Brands and agencies are already building capabilities to measure presence in chatbot answers as users shift behavior.

You don’t need perfection—just a management system:

Do we appear in generative comparisons for our core category terms?

Which attributes are associated with us?

Which sources are being used?

Where are competitors over-indexing?

5) Put governance around the narrative Treat positioning like a product: version control, update cadence, ownership, and accountability.

Because in an LLM world, inconsistency is a tax you pay every day.

The strategic reframing: the competition is now for inclusion, not attention

For a decade, enterprise marketing optimized for:

awareness,

clicks,

MQL volume,

and conversion rate.

In 2026, the scarcity is different. It’s market access—the right to be considered in a buyer journey that increasingly begins inside an LLM.

So here’s the cleanest way to say it to your CEO and CFO:

Not investing is not savings. It’s deferred erosion. Investing is efficiency recovery—with upside.

And that’s the reset. You can keep running your 2026 plan like it’s a marketing upgrade cycle. Or you can treat it like what it is: a market-access reset that will reward the vendors who become discoverable, defensible, and easy to choose—inside the answer economy.